[ad_1]

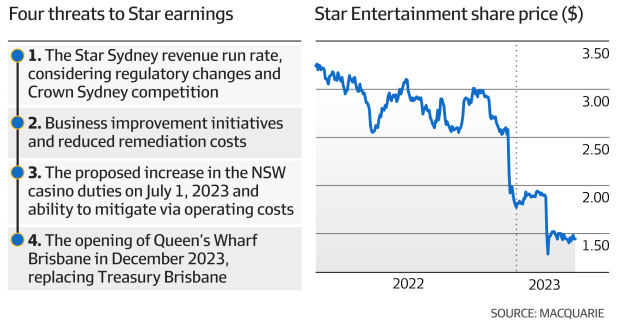

Star’s inventory is wallowing round $1.44 a share, with the newest hunch from the $1.73 stage on February 10 pushed by Star flagging a $1.26 billion loss forward of its interim outcomes. Before that, the inventory was de-rated from its $2.58 stage on December 16 after the NSW authorities slapped an estimated additional $100 million tax on its Sydney on line casino allow.

Five of 13 analysts price Star a “buy” together with Macquarie, JPMorgan, and Morningstar. Six brokers have “hold” calls in place, and CLSA and Barclay Pearce Capital are advising purchasers to “sell” the shares. The total value goal for the inventory is $1.58, based on Bloomberg.

Macquarie estimates Star’s EBITDA to be $310 million within the 2024 monetary yr, whereas JPMorgan and Morningstar anticipate the determine to be nearer to $422 million.

Last week, Star elevated David Foster to chairman, finishing a clear out of the board a yr after the damning Bell Review into Star’s sprawling Sydney on line casino kicked off.

The NSW evaluation helmed by Adam Bell, SC, discovered Star unfit to run the Sydney on line casino after turning a blind eye to organised crime gangs playing there, and permitting billions of {dollars} to be laundered by way of the gaming flooring.

But crucially, Star has been allowed to maintain its all-important licences, with little signal from NSW or Queensland of an urge for food to strip it of its permits regardless of being discovered unfit to run them.

Still, Star Sydney’s woes stay vital.

Competition

Crown Sydney luring excessive rollers to its gaming rooms atop the Barangaroo tower is a key risk that can form Star’s earnings, analysts observe.

Star Sydney’s half-year outcomes already present competitors with Crown is biting with income rising 127 per cent to $541 million, however remaining 14 per cent decrease than earlier than the pandemic.

The firm’s chief government, Robbie Cooke, mentioned that was as a result of competitors from Crown Sydney, excluding gamblers liable to cash laundering, and never offering complimentary alcohol in non-public gaming rooms.

“We continue to see The Star Sydney earnings re-basing with effectively only four months impact from regulatory change and Crown Sydney competition within the 1H FY23 result,” Macquarie says.

“Within our forecasts we have annualised the impact but continue to monitor the evolving regulatory and competitive environment. We continue to expect subdued table volumes, whereas slots look to be more resilient.”

Overhaul prices

The on line casino outfit is banking on some excessive curler volumes returning throughout FY24 “which is where there is the lowest visibility,” Macquarie noticed, including that Star mentioned it could ship $40 million in enterprise enhancements by way of the 2024 monetary yr, which included each working prices and income advantages.

Star simply accomplished an $800 million equity raise from buyers who have been backing it to outlive a wave of huge fines and potential increased taxes.

The proceeds of the $800 million fairness elevate will probably be used to cut back debt and pay penalties referring to the monetary crime watchdog’s costs in opposition to Star for permitting billions of {dollars} to clean by way of the on line casino’s gaming rooms with out correct checks on patrons.

Star estimated the corporate must pay $150 million, however Macquarie analysts anticipated it to be virtually double, “closer to $300 million”.

In addition to the AUSTRAC fines, Star additionally faces a compensation invoice if the Victorian Supreme Court sides with bitter shareholders, who’ve lobbed 4 separate class actions alleging Star misled the market about its compliance with anti-money laundering and counter-terrorism financing obligations.

How Star digests the proposed enhance within the NSW on line casino duties on July 1 and talent to mitigate this by way of working prices is the third issue that can form Star’s earnings.

Morningstar analyst Angus Hewitt expects Star will take a $100 million hit to earnings from the tax. But Macquarie estimates assume a $75 million web earnings affect and $65 million web cashflow affect. That’s based mostly on a $25 million discount in working prices and $10 million discount in capex.

Queen’s Wharf Brisbane due in December 2023, changing Treasury Brisbane, is the fourth ingredient weighing on analysts’ calculations.

Macquarie says it expects a four-year ramping interval, with monetary yr 2027 earnings at $300 million. But the 50 per cent possession construction of Queen’s Wharf means it can guide a separate administration payment which the dealer views as “exceeding $100 million in time”.

[adinserter block=”4″]

[ad_2]

Source link